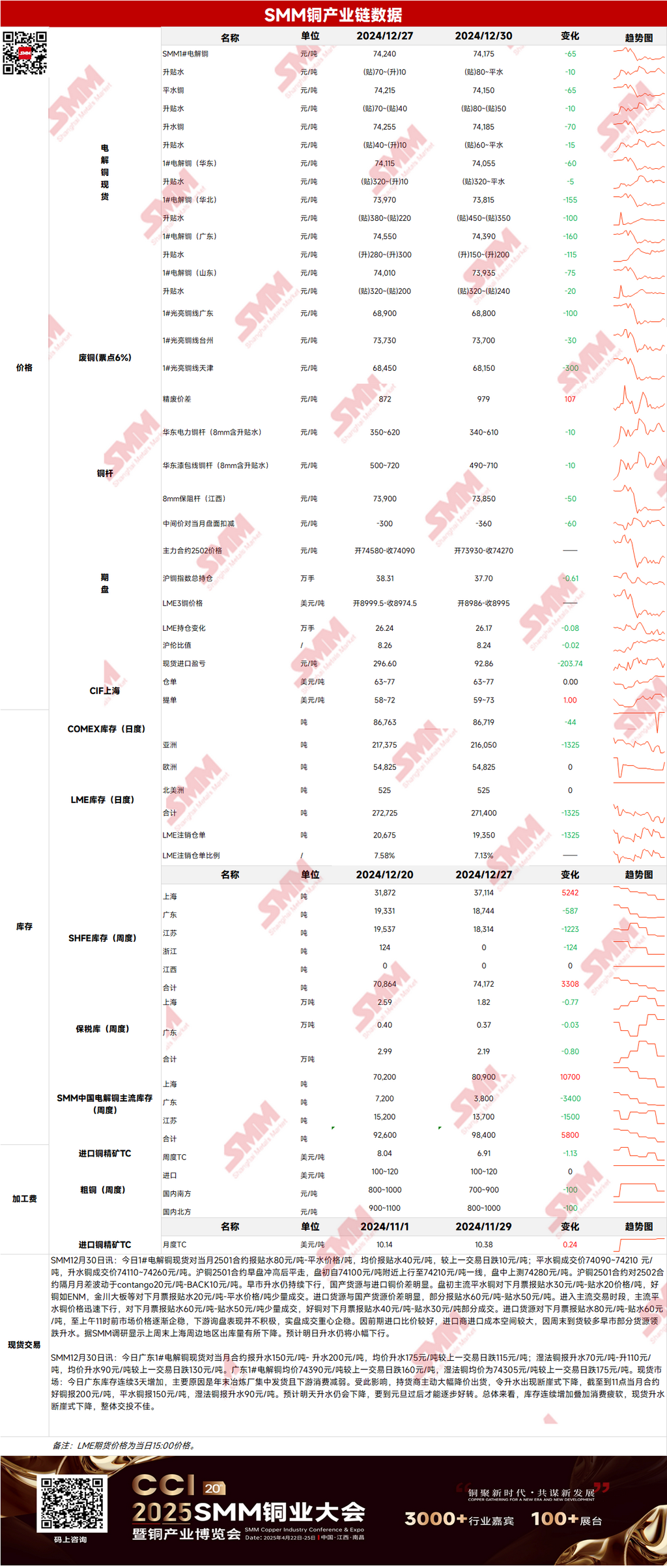

Futures Market: Overnight, LME copper opened at $8,961.5/mt, initially hitting a high of $8,966/mt before fluctuating downward throughout the session, touching a low of $8,905.5/mt. It slightly rebounded by the close, settling at $8,933.5/mt, with open interest reaching 262,000 lots. Meanwhile, the most-traded SHFE copper 2502 contract opened at 73,960 yuan/mt, initially hitting a high of 74,010 yuan/mt before fluctuating downward, touching a low of 73,740 yuan/mt by the close, and finally settling at 73,770 yuan/mt, down 0.54%. Trading volume reached 24,000 lots, and open interest stood at 150,000 lots.

【SMM Copper Morning Brief】News: (1) According to the latest CME FedWatch Tool, the probability of the US Fed keeping interest rates unchanged in January next year is close to 90%. Following the hawkish rate cut in December, market expectations have gradually shifted towards a slowdown or halt in easing in H1 next year, with global liquidity turning tighter.

(2) As of Monday, December 30, SMM copper inventories in major regions across China increased by 7,700 mt from last Thursday to 113,100 mt.

Spot Market: (1) Shanghai: On December 30, #1 copper cathode spot prices against the front-month 2501 contract were quoted at a discount of 80 yuan/mt to parity, with an average price at a discount of 40 yuan/mt, down 10 yuan/mt from the previous trading day. Due to favorable SHFE/LME price ratios earlier, importers had larger cost margins, and the significant arrivals over the weekend led to some sources dragging down premiums in the early session. According to an SMM survey, outflows from warehouses in areas surrounding Shanghai decreased over the weekend. Spot premiums are expected to decline slightly today.

(2) Guangdong: On December 30, #1 copper cathode spot prices against the front-month contract were quoted at premiums of 150-200 yuan/mt, with an average premium of 175 yuan/mt, down 115 yuan/mt from the previous trading day. Overall, continuous inventory increases combined with weak consumption led to a sharp decline in spot premiums, with overall trading activity remaining sluggish.

(3) Imported Copper: On December 30, warehouse warrant prices were quoted at $63-77/mt, QP January, with the average price unchanged from the previous trading day. B/L prices were quoted at $59-73/mt, QP January, with the average price up $1/mt from the previous trading day. EQ copper (CIF B/L) was quoted at $13-27/mt, QP January, with the average price unchanged from the previous trading day. These quotes referenced cargoes arriving in early January. Yesterday, the SHFE/LME price ratio for the SHFE copper 2501 contract was around +23 yuan/mt. LME copper 3M-Jan was at C$82.86/mt, while the SHFE copper 2501-2502 spread was around C$43/mt. Ahead of the New Year holiday, some suppliers were less active in spot trading due to holidays and bank settlements, resulting in fewer offers. However, downstream demand remained urgent, leading to higher offers for near-port B/L and warehouse warrants. EQ B/L quotes also rose, but overall transactions remained inactive.

(4) Secondary Copper: On December 30, secondary copper raw material prices fell by 100 yuan/mt MoM. Guangdong bare bright copper prices were quoted at 68,700-68,900 yuan/mt, down 100 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 979 yuan/mt, up 107 yuan/mt MoM. The price difference for rods was 835 yuan/mt. According to an SMM survey, secondary copper raw material prices in north China declined slightly more than in south China. Weak consumption, combined with growing concerns among suppliers about policy impacts on prices, led some suppliers to offload inventory to avoid unnecessary losses. Some suppliers aimed to reduce secondary copper raw material inventories before the year-end.

(5) Inventory: On December 30, LME copper cathode inventories decreased by 1,325 mt to 271,400 mt. SHFE warehouse warrant inventories increased by 4,173 mt to 17,184 mt.

Prices: Macro-wise, the US dollar index hovered at highs on expectations for Trump's policies, weighing on copper prices. Domestically, the bond issuance volume of three policy banks in Q1 next year is expected to hit a record high. On the fundamentals side, both imported and domestic copper arrivals increased over the weekend, while consumption remained weak near the year-end. As of Monday, December 30, SMM copper inventories in major regions across China increased by 7,700 mt from last Thursday to 113,100 mt. Overall, with weak year-end consumption and rising inventories, copper price gains are expected to be limited today.

Click here to view the SMM Metal Database.

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】